In-Depth Look: Why WELL Health Technologies Corp. - $WELL.TO is a Strong Investment

In-Depth Look: Why WELL Health Technologies Corp. - $WELL.TO is a Strong Investment

This post gives a brief synopsis on why WELL Health Technologies is a current core holding in Brandon's Portfolio.

Overview/Business Model:

WELL Health technologies has an incredible business model and is demonstrating incredible growth rates both organically and through acquisitions. WELL is Canada’s largest outpatient medical clinic owner-operator and leading multi-disciplinary telehealth service provider.

First and foremost, WELL’s mission is to help medical practitioners to support their business, and patients in the hopes of positively impacting healthcare outcomes. Other than the Canadian government itself, WELL Health has the most Comprehensive end-to-end healthcare system in Canada.

WELL Health may be a tech stock, but its primary focus is to assist the healthcare industry a typically defensive sector. Despite the growth slowdown in tech, WELL Health Technologies, unlike its peers hasn't seen a slowdown in its growth & Its margins have not compressed, rather the opposite its recording record margins and showing impressive resilience.

Practitioner Enablement Platform:

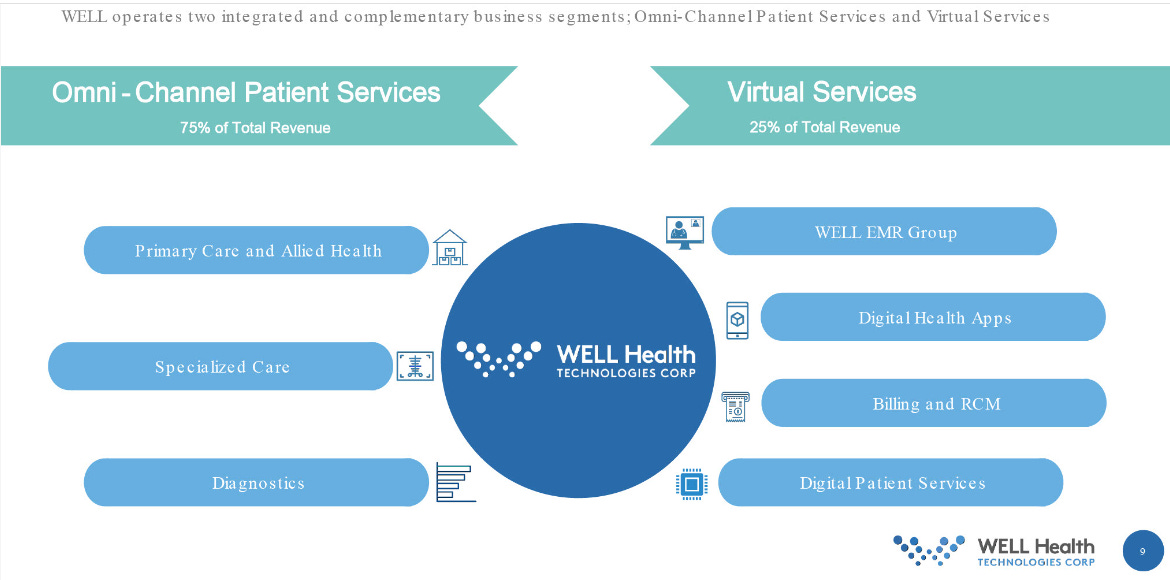

WELL’s business operates in 2 segments, their practitioner enablement platform, and omnichannel services. Their practitioner enablement platform offers digital healthcare solutions for medical clinics and healthcare practitioners worldwide. Solutions offered through the platform include Electronic Medical Records (EMR) SaaS, practice management software, practitioner enablement tools, digital health apps that extend the features of EMRs, billing, and Revenue Cycle Management (RCM) solutions, patient engagement technologies, clinic optimization tools, cybersecurity solutions, and more. Substantial value is created on the practitioner’s end.

WELL’s practice management platform is designed to aid healthcare providers that work within WELL’s outpatient medical clinic network as well as practitioners who work outside of this network in the thousands of clinics globally.

Omnichannel:

WELL is also Canada’s largest outpatient medical clinic owner-operator and leading multi-disciplinary telehealth service provider. The company has its own medical clinic network with locations in Canada and the U.S. This network consists of outpatient medical clinics serving primary, secondary, diagnostic, executive, and specialized healthcare services.

WELL Health is an omnichannel digital health provider meaning they offer healthcare solutions through a wide variety of mediums. They own and operate a range of assets including medical care facilities and virtual healthcare or telehealth operations both in Canada and the United States.

Medical Care facilities are the type of businesses with inelastic demand. If people need medical treatment they will get it and WELL is providing solutions to make life a lot less complicated on the end of the patient and the practitioner.

Canada’s Struggling HealthCare System needs Innovation:

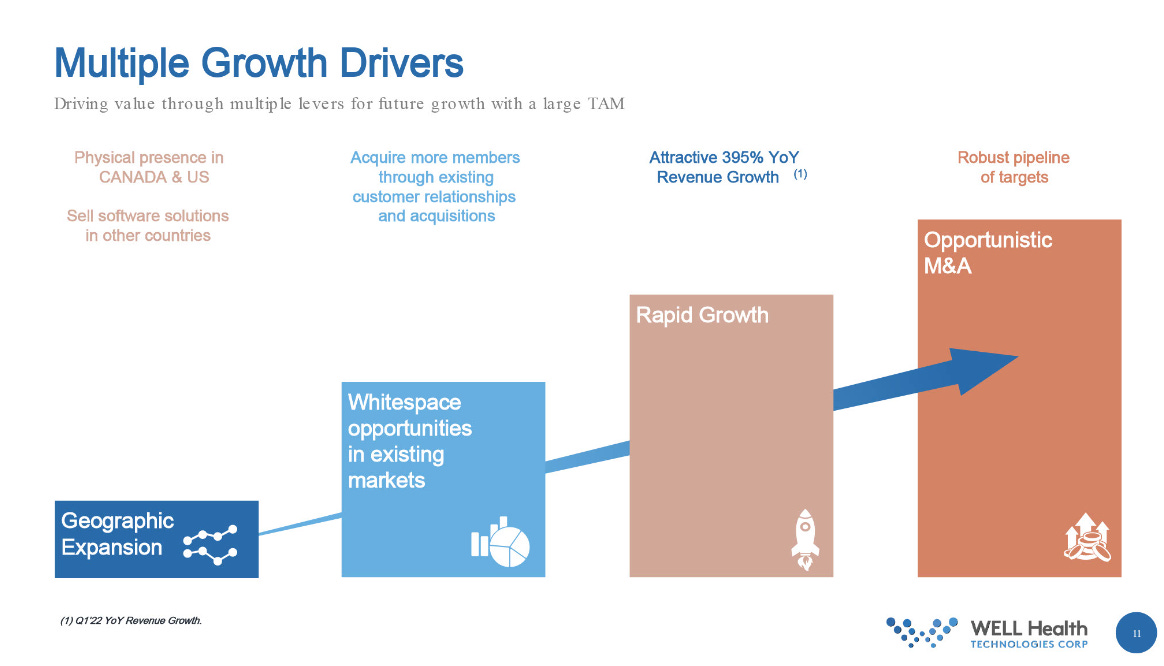

Canada’s healthcare system is fragmented and under-digitized. WELL’s mission is to develop and scale a healthcare system where patients around the world have greater access to a variety of services, and where all healthcare practitioners can work with the aid of technology designed to enhance their delivery of healthcare. The industry suffers from interoperability challenges. WELL aims to continue increasing the scale of its business through different processes. Some include integrating technology into its own practices or expanding its medical clinic network.

Current Crisis – Shortage of Healthcare Workers.

There is an extraordinary shortage of healthcare practitioners across Canada. Healthcare workers across all professions including nurses, long-term care, home support workers, paramedic, and doctors have been overworked for the last 2 and a half years. They have come under an extreme amount of stress and are burnt out which has led them to consider leaving their job.

Healthcare workers are now cutting hours, leaving public jobs, or simply retiring because their workloads have become overwhelming. As we know this problem snowballs because the nurses that remain must take on the workloads of all those who leave subsequently causing them to burn out and quit which prevents Canadians from getting the health care they need in a timely manner.

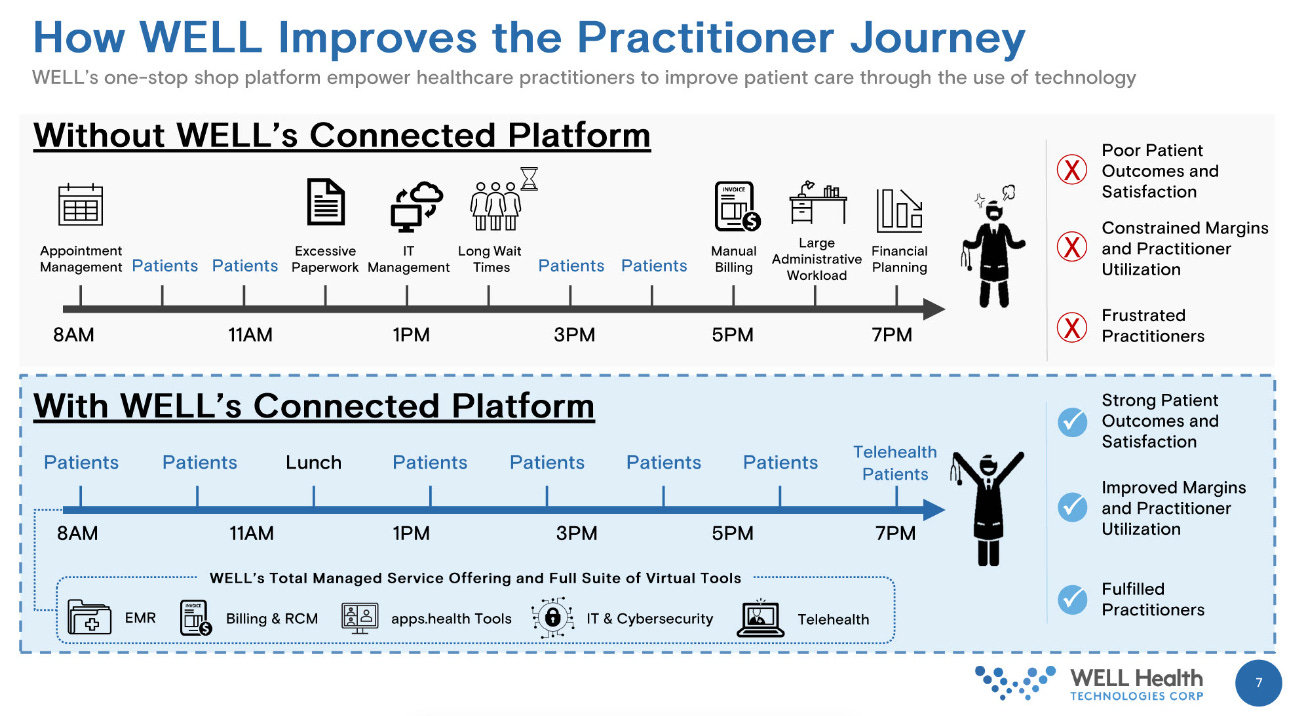

WELL has designed products and services that will assist healthcare professionals by digitizing administrative tasks. They have developed technology to mitigate inefficiencies that are time-consuming, complex, and tedious which allows practitioners to focus more time and energy on doing what they do best which is caring for their patients.

CEO Hamed Shahbazi:

“WELL’s business model of ‘caring for the care providers’ by supporting them in all aspects of running their operations and allow them to focus on providing care is working. Now more than ever, at a time when healthcare workers are under duress, WELL is applying all of its talents and resources to help them focus on what matters, providing the best patient care available and delivering optimal health outcomes.” – Q2 Earnings Call.

Management:

WELL Health has one of the most competent management teams in the industry. When it comes to investor calls, they are transparent in their growth targets and continue to exceed analyst expectations. They have all worked together in the past and are known for building highly scalable businesses. The CEO of WELL Hamed Shahbazi created his first startup and sold it to $PYPL for $300M then subsequently started WELL Health technologies.

Competitive Advantages:

WELL’s first-mover advantage and highly efficient business model have put them in a superior position to the competition. They offer a full suite of products and services that have inelastic demand. The state of the economy and personal finance doesn’t affect consumers’ need for health care services and recession or not people will seek medical attention if they need it. 1/5 medical practitioners in Canada use a WELL health product or service. In Canada they are the industry leader in:

Telehealth but WELL Health is not Teledoc:

The Pandemic taught us the Global Healthcare system must be more efficient than it is today. Covid-19 forced doctors to have phone call consultations, instead of in-person treatment. This was a sudden change for patients, and some felt as though they didn’t couldn’t receive the proper treatment.

That’s where telehealth solutions come in. Companies like WELL Health Technologies can also provide platforms that healthcare providers can use to see patients virtually. In addition, WELL Health also maintains an online marketplace that healthcare providers can use to obtain different apps. The telehealth industry is still a very new area and could look very different in 10 years’ time. However, WELL Health is shaping up to be a solid player in that space.

What separates WELL Health from other telehealth companies is its full suite of other products and services. It offers cybersecurity, billing, and EMR services that telehealth providers can use to improve their own businesses. The global EMR (electronic medical record) industry is worth approximately $28 billion and is expected to reach $48 billion in 2028 as of now WELL has a top 3 EMR Telehealth Platform in Canada with the #1 EMR App Ecosystem and they also provide many other services.

It offers cybersecurity, billing, and EMR services that telehealth providers can use to improve their own offerings. - EMR (electronic medical record) App Ecosystem. it is estimated that the global EMR industry is worth approximately $28 billion and is expected to reach $48 billion in 2028 as of now WELL has a top 3 EMR Telehealth Platform in Canada.

Rob Goff, Echelon Markets Analyst:

“We continue to be encouraged by the success of WELL’s US growth assets Circle and Wisp, especially at a time when US bellwether Teledoc has been challenged by competitive pressures within its direct-to-consumer (DTC) telehealth segment early in 2022…Those challenges led to Teledoc slashing its 2022 revenues/EBITDA guidance with the Q122 release; meanwhile, Circle and Wisp continue to accelerate and have generated positive EBITDA for several months now despite WELL’s focused marketing reinvestment into the growth assets, prioritizing scale over profitability,” – Cantech Letter

Some analysts believe that with the Pandemic now behind us, WELL Health will severely underperform as the economy reopens. One aspect of WELL Health that separates them from peers such as TDOC 0.00%↑ is that they use an omnichannel method and outpatient clinics with inelastic demand which acts as a hedge to their overall business. Further, it seems like WELL Health is having stronger organic growth than its peers.

CEO Hamed Shahbazi:

"Our organic growth remained strong in Q4 at over 10% for the entire business. This strong growth was driven through our services business with over 50% organic growth, which we believe is sustainable and will lead our overall organic growth story in 2022 and beyond." – Q2 Earnings Call

Bought Deal offering:

In Q1 WELL announced it had completed a $30-million bought deal offering, with the lead order coming from Hong Kong billionaire and philanthropist Li Ka-Shing who already had a substantial position in the company. The company made a smart decision to raise capital during a market downturn so that they have the resources available for strategic acquisitions if the opportunity presented itself. Now that valuations have substantially come in, they believe they can go deal hunting.

Acquisition Strategy:

WELL actively acquires physical and digital assets to vertically integrate into its healthcare network. WELL Health’s rapid growth has been fueled by approximately 20 strategic acquisitions. For example, in 2021, WELL acquired CRH Medical in a deal worth about $369 million, their largest acquisition to date. CRH is an American company that provides treatment solutions for gastrointestinal diseases. Other acquisitions include WISP, Uptown Health, MyHealth, CognisantMD, and Jasper Anesthesia Care.

The company’s most recent acquisition was Calgary-based healthcare provider INLIV which specializes in consumer preventative health, corporate and executive health, primary care, cosmetics, fitness, and integrated health services. INLIV had TTM revenue of $7.3 million 85% recurring, and 1,000 customers.

Chief Medical Officer, Dr. Michael Frankel:

“INLIV has an excellent track record in providing outstanding patient care,” “We are very excited about adding them to our network as this planned acquisition represents the continued execution of our plans to further grow our presence in the premium corporate and executive health segment. We are intent on continuing to establish our technology enabled clinical group across the country.” - Investor Relations

Reinvestment Strategy:

One of Warren Buffet's crucial investing lessons is to Invest in companies that can reinvest a lot in organic growth such as WELL Health. Invest in companies that can reinvest their earnings in organic growth for years or even decades, the earnings of the company will explode over time. For WELL, Reinvestment is also a top priority:

"The cashflows generated by the Company will continue to be re-invested in the business and allocated in a disciplined manner, which may come in the form of further acquisitions, share repurchases, or to accelerate organic growth." – Q2 Earnings Release Investor Relations

Q2 Results, Another Record Quarter and Full Year Guide:

WELL ER Highlights, they killed it yet again.

WELL achieved record quarterly revenues of $140.3 million in Q2 2022 resenting a 127% YoY increase compared to Q2 2021

Adjusted Net Income of $17.2 million in Q2 2022, compared to Adjusted Net Loss of $1.2 million in Q2-2021.

Record Adjusted EBITDA of $26.4 million in Q2 2022, compared to Adjusted EBITDA of $11.9 million for Q2 2021.

Omni-channel Patient Services revenue increased 88%

Virtual Services revenues increased 281% These results were driven by accelerating organic growth.

Record Adjusted Gross Profit of $75.5 million in Q2-2022, compared to Adjusted Gross Profit of $30.2 million in Q2-2021, an increase of 150%.

Adjusted Gross Margin of 53.8% during Q2-2022 compared to Adjusted Gross Margin percentage of 48.9% in Q2-2021.

Adjusted EBITDA was a record $26.4 million for Q2-2022, compared to Adjusted EBITDA of $11.9 million in Q2-2022, an increase of 122%

CFO Eva Fong:

“I am also pleased to report that WELL is a profitable business that generated $15.4 million free cash flow attributable to shareholders in Q2 which can be used to fund the Company’s future organic and in-organic growth.” - Q2 Earnings Press Release

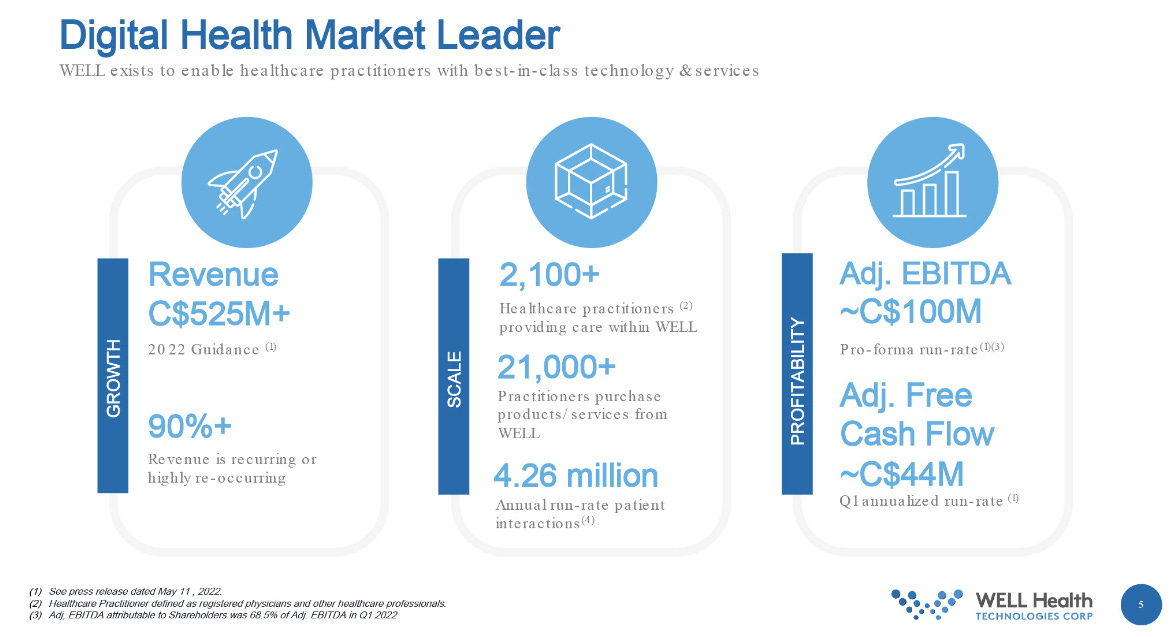

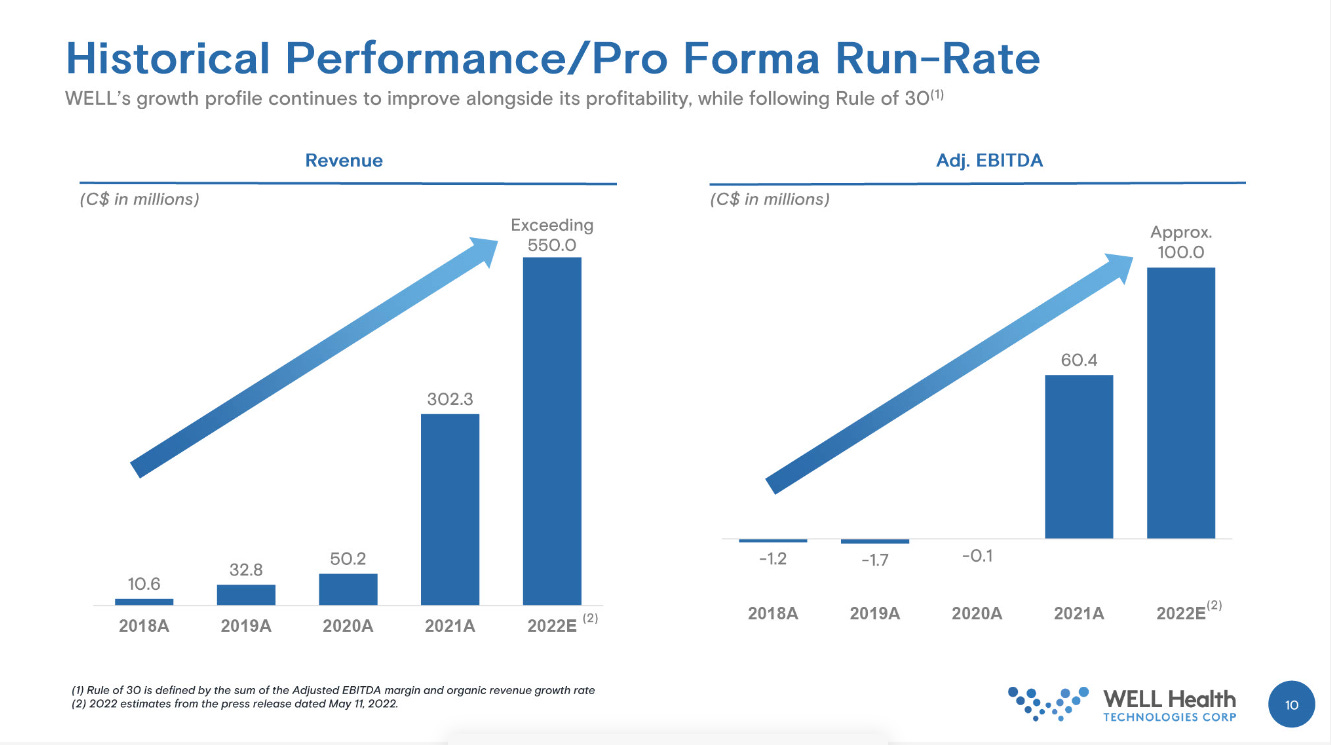

For the third consecutive quarter where WELL has raised its revenue guidance. WELL’s outlook for 2022 remains strong and resilient. WELL expects 2022 annual revenue to exceed $550 million, compared to the previous guidance for annual revenue exceeding $525 million. WELL Health also expects Adjusted EBITDA of approximately $100M for the full year.

Financials/Valuation

WELL Health reports its results using Non-GAAP and GAAP measures but, in their press releases, they report Gross Profit, EBITDA, and Net Income on an adjusted basis and define FCF as Free Cash Flow attributable to shareholders. Some investors get concerned when a company plays with its financials as they think management is trying to portray numbers that are not exactly accurate but rather make the results look better.

In the case of WELL Health, reporting this way gives a much better representation of how the underlying business is performing and excludes items that don’t influence operations. For example, the Company defines Adjusted Net Income as net income, after excluding the effects of stock-based compensation expense or amortization of acquired intangibles. WELL believes Adjusted Net Income is a financial metric that tracks the earning power of the business available to WELL shareholders.

WELL, Health currently has ~ $365M in total debt. Adding the current and non-current Loans and borrowings, Lease liabilities, and convertible debentures to get the total. Subtracting the $57.13M in cash and short-term investments we get the net debt of $307.75M in net debt. Considering the $15.4M (and growing) in FCF attributable to shareholders vs the $5.25M in interest expense in the quarter, they are well covered.

If WELL can meet its goal of $550M in revenue this year, then at its current market cap of ~$850M they are trading at a P/S of ~1.5 which is quite low compared to its high-growth technology peers. WELL expects to be profitable for the full year 2022, on an adjusted net income basis. It is also expected that the combined businesses of Circle Medical and WISP will exceed $130 million in sales on a run-rate basis later this year.

Investors should not use adjusted financials as a replacement for actual financials, but for right now it gives the best indication of how management believes the core business should be valued. $100M in adjusted EBITDA at WELL’s current market cap translate to an EV/EBITDA multiple of ~8.5x much lower than some of its competitors where the average is around 17-18x.

My DCF valuation of WELL brings the company’s intrinsic value close to $13.5 suggesting a 250% upside from its current price of $3.70. I think Well Health got caught up in the frantic selling of anything related to risk. All tech stocks got thrown out with the garbage even if they possessed strong financials and growth potential. Over the last 4 years from 2018 to the end of 2021 WELL grew revenues at a 131% CAGR. On a Price to earnings growth or PEG ratio basis, you could argue it’s undervalued.

Risks:

WELL, Health’s acquisition growth is impressive, but it also poses a challenge to management on whether they can integrate all these businesses successfully and efficiently into their network. The eventual goal is to accelerate organic growth, expand margins and grow cash flow. We will need to assess the coming quarters to see if these acquisitions are performing well and fueling growth.

We cannot ignore the impacts that a recession has on technology businesses. Rising rates destroy unprofitable companies that rely on debt financing and low-interest rates. Economic growth slows, which usually leads to high unemployment and depressed consumer sentiment. During a recession, patients will likely postpone medical treatments that are not urgent. However, Canadian’s healthcare is covered by their insurance.

One thing I would highlight is that the Company does not see any material influences or challenges that would impair its ability to deliver a strong outlook in 2022. Healthcare for the most part is considered “recession-proof” and $WELL has a hedged business model and a strong balance sheet. WELL’s business does not depend on any outside factors and with most of their business in North America, WELL is quite insulated from any geopolitical effects.

Technicals:

WELL has been trading in this falling wedge suggesting the selling pressure is losing momentum. I believe the price will eventually catch up to fundamentals.

Conclusion:

This company will become the largest vertically integrated Digital Healthcare/Healthcare technology company in Canada with the ability to grow just as fast in the U.S. The prospects of this company are bright, and its diversified income stream gives them a competitive advantage over industry peers.

I think this company has all the necessary tools to have a positive impact on the current shortage of healthcare workers. They consistently beat analyst estimates and continue to have record quarters. WELL Health technologies is developing products and services for the inevitably changing healthcare system positioning themselves to be a dominant player.

Their products provide valuable services for practitioners and patients and their network will continue to grow as more people begin to see its importance. I think WELL sticks out as a clear winner demonstrating rapid growth, scale, and profitability.

If you enjoyed the read and are interested in more company research like this, please be sure to subscribe to this Substack and share this post with other investors.