In-Depth Look: Why Meta Platforms, Inc. - $META Is a Strong Investment

In-Depth Look: Why Meta Platforms, Inc. - $META Is a Strong Investment

This post gives a brief synopsis on why Meta Platforms is a current holding in Brandon's Portfolio.

Overview/Thesis

META 0.00%↑ is a high-margin monopoly business with strong network effects that trades like a coal company. the ad industry has seen a major slowdown and companies are preparing for coming challenges by issuing profit warnings. Ad-tech names have been hit hard which has resulted in META 0.00%↑ losing ~ 47% year to date. META 0.00%↑ has also announced its first major hiring freeze across several divisions. In recent months lot of Investors have become extremely pessimistic towards META 0.00%↑. They hate it as an investment, the products, Zuckerberg. Some see investing in $META as unethical and refuse to do so, but I am investing to make money and I choose to ignore the noise. Everybody hates Mark Zuckerberg but he's much more competent than people give him credit for. They have also recently shifted focus to engagement on short-format videos with Reels.

Advertising Ecosystem:

The ad-tech space operates as a duopoly shared by META 0.00%↑ & GOOG 0.00%↑ with AMZN 0.00%↑ gaining some traction. Digital ad spending will continue to grow over time. I highlighted in my article about Digital Turbine a study by eMarketer, indicating that Global Digital Ad Spend is projected to grow to ~$876.10 Billion by 2026, which represents an ~11% CAGR. Digital advertising will continue to take a share of overall ad spending from traditional. Advertising drives the consumer and thus forces businesses to allocate larger amounts of capital toward advertising their products/services to retain the consumer’s attention.

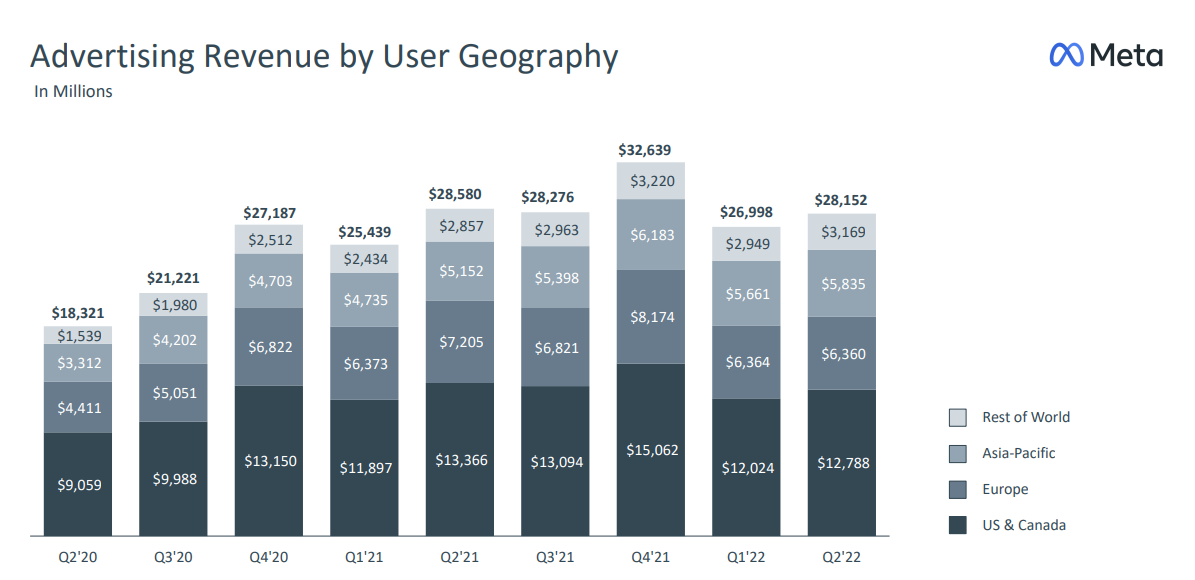

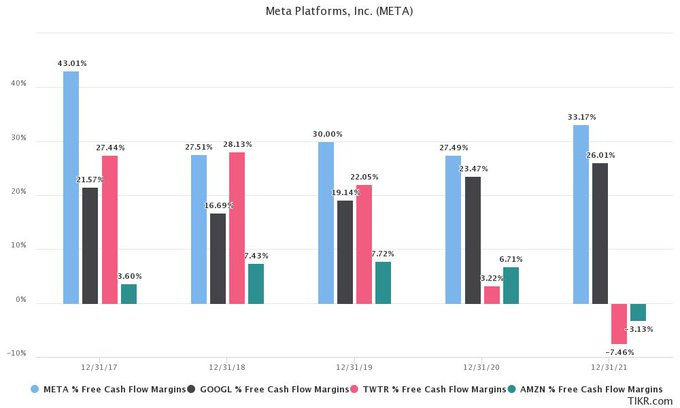

We come across thousands of advertisements daily. Another study detailed that on average, individuals encounter more than 4000 advertisements each day. At first glance it looks alarming, however, it makes a lot of sense if you consider all the advertising mediums around us from TV to social media, podcasts, etc. Digital advertising trends are only growing stronger over time. For companies like META 0.00%↑, it’s all about occupying the most on-screen real estate. Those that will benefit from this trend are the ones that offer services and platforms that can attract and retain the most eyeballs. Ad-spend will ramp back up once the uncertainty surrounding a U.S recession and historically low consumer sentiment fades. Ad-spend will likely concentrate on only the most successful publishers like META 0.00%↑, GOOG 0.00%↑, AMZN 0.00%↑ & TikTok for now. SNAP 0.00%↑ released their earnings before other ad-tech names and posted atrocious results which led many to conclude Snapchat was the canary in the coal mine for all ad-tech stocks. We later realized this was false and was more company-specific than industry-wide. Although we saw a decline YoY from Q2 2021, META 0.00%↑’s still posted strong advertising revenue despite the broader economic slowdown. The average price per ad fell due to a reduction in advertiser demand. META 0.00%↑ did not perform as well as GOOG 0.00%↑in Q2 on a YoY basis. You can see this as META 0.00%↑’s Ad Revenues were down 1.5% YoY while GOOG 0.00%↑’s were up 11.6%.

Growing Users:

Highlights from their Q2 ER:

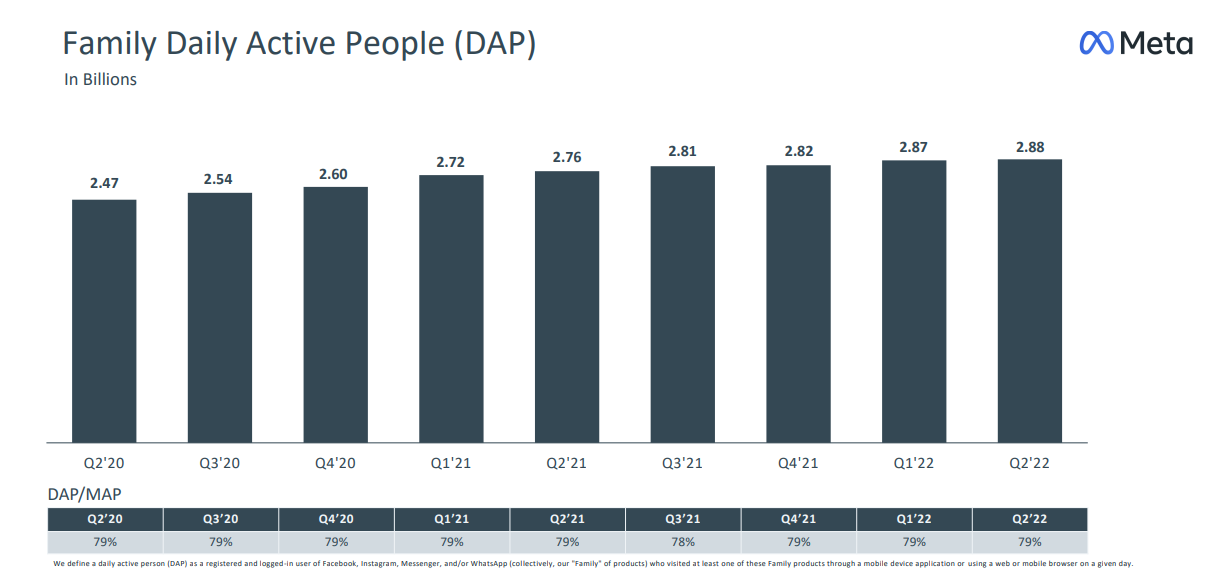

Family daily active people (DAP) 2.88B an increase of 4% YoY.

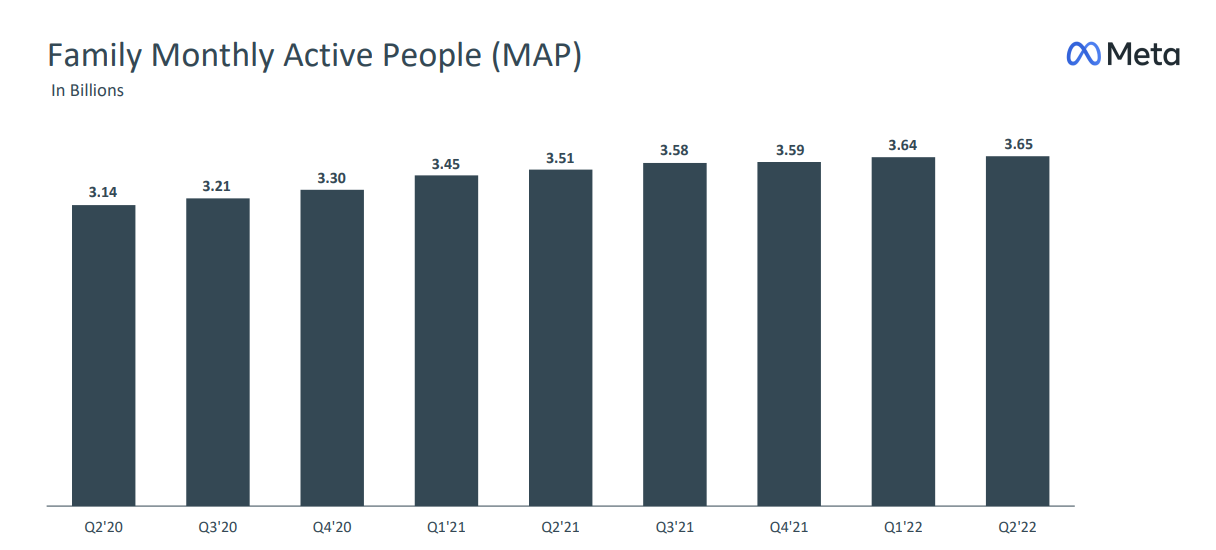

Family monthly active people (MAP) 3.65B an increase of 4% YoY.

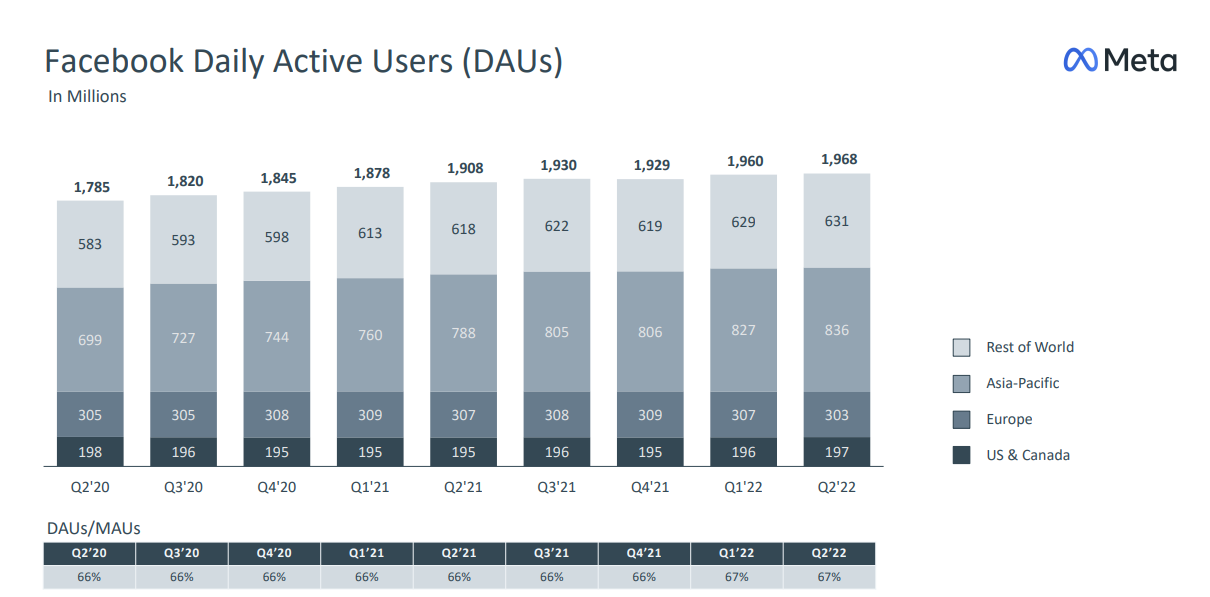

Facebook daily active users (DAUs) 1.97B an increase of 3% YoY.

Facebook monthly active users (MAUs) 2.93B an increase of 1% YoY.

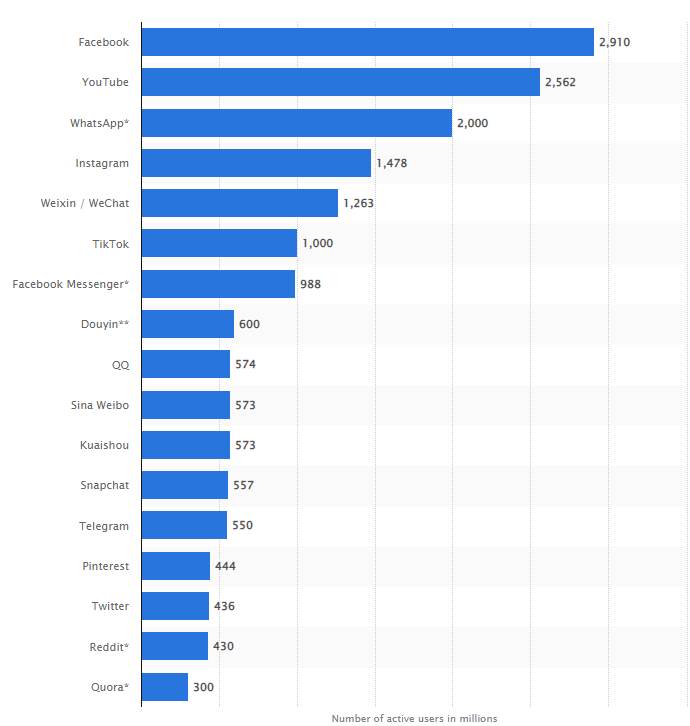

It is also worth noting the investments being made to build massive subsea fiber optic cables around Africa which will bring internet infrastructure to millions. META 0.00%↑ & GOOGL 0.00%↑ are at the forefront of this. Africa has 1.4B inhabitants and they are the least connected continent. META 0.00%↑ has a huge lead when it comes to active users compared to other social media sites. META 0.00%↑ owns 4 of the top 7 most popular social media sites which gives it a huge lead over competitors for network effects.

Metaverse:

Everyone has their own theory of what the metaverse may look like 5-10 years from now. Will it be dead or multiples larger than it is today? When it comes to Zuckerberg’s vision, I have a feeling one day everyone will look back on his original investment into VR & AR and only talk about how genius it was that he innovated ahead of the competition. I bet there will be significant barriers to entry in this new industry and META 0.00%↑ is looking to be the dominant player. You may hate Zuckerberg, but the guy delivers time and time again, and META 0.00%↑ gearing up to be the #1 player in the Metaverse if his vision ends up working out. his ideas are 5-10 years ahead of Wall Street analysts. The largest companies in the world like AAPL 0.00%↑ and MSFT 0.00%↑ are making investments in the Metaverse yet people still believe the whole concept is fake and overhyped. As of right now Reality labs is bringing down the company’s net income and making up a substantial portion of Capital expenditures. In addition, Zuckerberg told staff that Apple will be a large Metaverse competitor. It’s a race for first-mover advantage, both have the resources and the capabilities to unlock substantial value with this new technology.

I think it's pretty clear that Apple is going to be a competitor for us, not just as a product but philosophically. We're approaching this in an open way and trying to build a more open ecosystem. We created the Metaverse Open Standards Group, and Apple didn't join.

Reality Labs will likely see a revenue spike in the back half of 2022 due to seasonality effects such as device purchases for holiday spending. I would highlight that the operating loss from the Reality Labs segment has declined for the last two quarters. The magnitude of investment is still not having a noticeable effect on overall revenue as it is still a very small percentage of META 0.00%↑’s overall revenue coming in at ~2%. As of right now, Reality Labs is a net negative for META 0.00%↑ because it is burning through cash and it is also a massive gamble, given that we have no idea what will become of the Metaverse, how it will look or function.

Reels Engagement:

Mark Zuckerberg revealed that META 0.00%↑ crossed a $1 Billion annual ad-revenue run rate for Reels. He also noted that Reels now has a higher revenue run rate than Facebook & Instagram Stories had when they first launched. Management mentioned that that time spent on Reels across Facebook and Instagram increased by more than 30% sequentially in Q2. Reels make up 20% of the time on Instagram and it’s growing as a percentage of time on Facebook. Overall, Reels was a net positive on the time users spent on META 0.00%↑’s Family of Apps but it did take away from time spent using other apps or features like stories. We know that META 0.00%↑’s success relies ultimately on their ability to maintain and engage as many users as possible because their business is to provide advertisers with the best platforms to promote their products/services and get noticeable results. Half the planet uses one of META 0.00%↑apps every month and ~ 1/3 of the planet uses one of their apps every day. This extraordinary moat will help them to continuously improve their AI and targeting technology and scale its existing user ecosystem of advertisers & content creators. META 0.00%↑’s valuation has been cut in half and I am convinced the risks surrounding TikTok competition, ad-spend weakness and apple IDFA changes have been sufficiently priced in. This valuation reset gives them time to execute on their road map to substantially scale Reels. Investors are waiting for management to prove that it can build a sustainable product.

CFO David Wehner:

On Reels engagement, we’re pleased with how that is progressing. We think that we’re doing well. Obviously, there’s third-party tracking services that provide data on TikTok and other services, but we feel that we’re competing very effectively in terms of rolling out Reels on Instagram and Facebook and on both its growing very quickly. And we saw, as Mark mentioned, 30 percent increase from the time that people spent engaging with Reels across both Facebook and Instagram. Clearly, it’s above 20 percent of the time on Instagram and it’s growing as a percentage of time on Facebook. So we think we’re on a good track with Reels.

We invest a lot in building infrastructure. And culturally, we focus on moving and learning faster than everyone else. And I think that those are sustainable advantages. And so certainly, I think that the AI technology infrastructure that we're building, I think it can compound and be better than others in the industry and that will be an advantage and make the product better over time. But I think at the end of the day, what that really comes down to is just I try to push the company to be one that learns faster and just keeps iterating and moving faster than we did in the past and then others in the industry do. And I think if we can do that well, then we'll continue to succeed. But I think the moment that we stop doing that, then we'll basically fall behind. It's a very competitive field and we need to keep on pushing ahead. But I think the reason why we have succeeded and seen so good results with Facebook, Instagram and the other social apps is because we basically focus pretty relentlessly on just pushing to constantly improve them.

TikTok Competition:

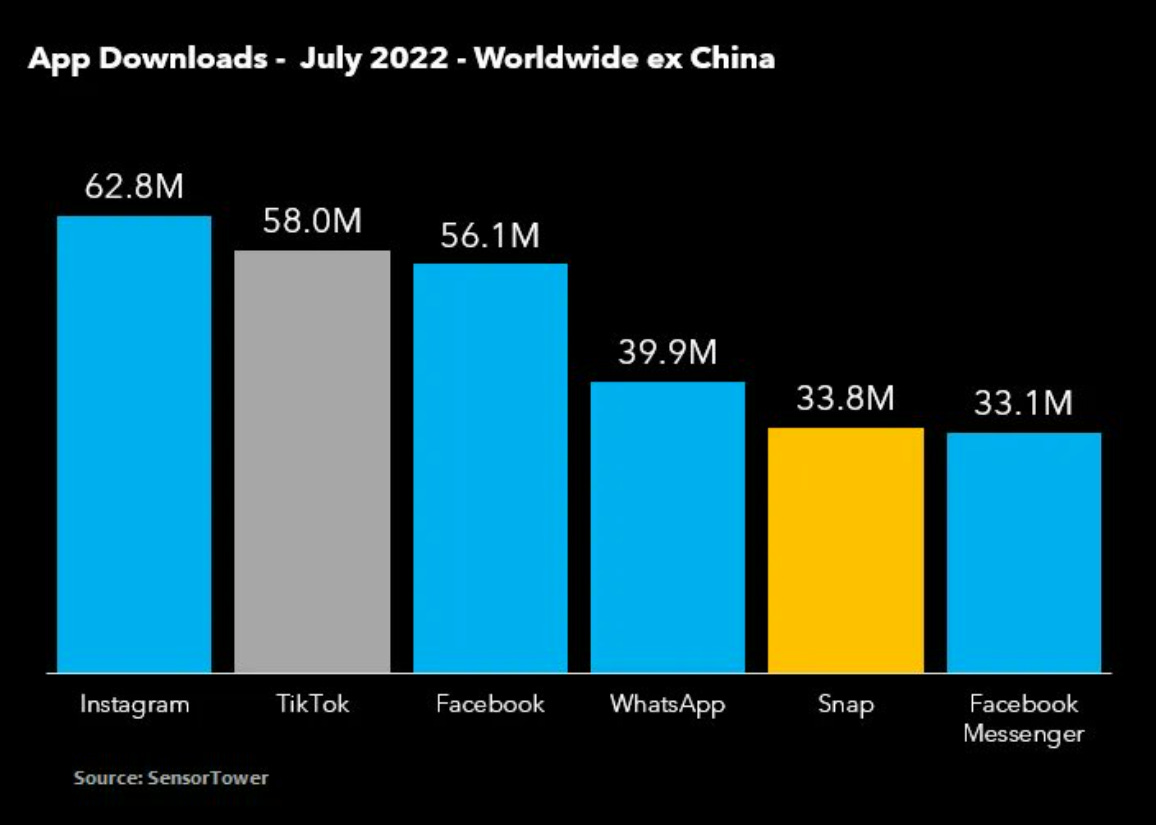

Despite TikTok’s growing user base and recent exponential growth Instagram still managed to post the most global App Downloads in the month of July and the other Apps by META 0.00%↑ were not far behind. Combined they have > 3x the downloads of TikTok. META 0.00%↑’s family of Apps are regularly in the top 10 even 5 most downloaded apps in the IOS and Google Play App stores every month. It was never mentioned by the CEO if Reels has closed the gap between TikTok at all but META 0.00%↑ is likely to prioritize growing Reels over other revenues. If analysts expect Ad-spend to be cut in a slowing growth environment, then TikTok will see a slowdown in their hyper-growth as well.

Apple IDFA Changes:

In April 2021, Apple updated IOS so that users will have the choice to opt-in to allowing ad-tracking by social media apps like Facebook and Twitter. This resulted in a $10 Billion hit on its top line in 2021. The update essentially just makes it difficult for social media companies to deliver targeted ads to their users. However, META 0.00%↑ has been working to develop solutions to improve its targeting as well as to make it easier for users to engage with businesses in the family of Apps. One of the solutions they have rolled out is Click-to-Messaging which management stated is a multi-billion-dollar business that continues to see strong double-digit YoY growth.

Incoming CFO Susan Li:

Apple’s IDFA (Identifier for Advertisers) changes remain a headwind to revenue and to things like measurement and targeting in Q2, but it was not a contributor to the sequential deceleration in year-over-year growth relative to Q1. And, in fact, we started to see a benefit to year-over-year growth throughout Q2 because we were lapping the increased adoption of iOS 14.5 from a year ago, and we’ll get a further tailwind in Q3 as we lap the full first quarter of iOS impact.”

Departing COO Sheryl Sandberg (Q1):

We’re also helping businesses connect directly with customers and grow more onsite data conversions through products like Click-to-Message ads. This is where you click on an ad in your Facebook or Instagram feed and it opens a chat with the business in Messenger, Instagram Direct or WhatsApp. It’s already a multi-billion dollar business, with healthy double digit year-over-year growth in Q1.

Financials/Valuation:

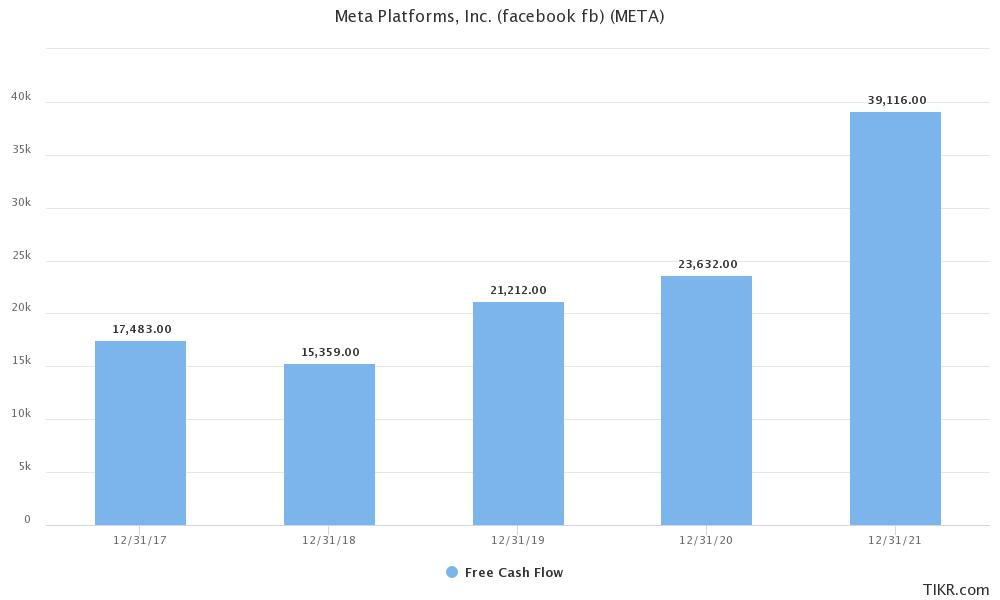

Since its IPO META 0.00%↑'s share price has moved in lockstep with its extraordinary rise in earnings and free cash flow. However, since August 2021, they have decoupled. META 0.00%↑ shares have dropped > 50%, while its free cash flow has increased > 60%. META 0.00%↑ now trades at a market cap of roughly $480 Billion, with a debt-free balance sheet and ~$40 Billion in cash and short-term investments. Purchasing the stock in and around these levels is essentially buying a stock within an industry that is in secular decline, which it isn't. Referencing this chart via Statista, their ARPU has been growing every year showing they can effectively monetize their massive user base.

META 0.00%↑ is expected to remain highly free cash flow (FCF) profitable. If there is one company with the resources and execution capabilities to navigate these headwinds, it has got to be META 0.00%↑. According to FinanceCharts.com over the past 5 years, META 0.00%↑ has a grown its revenue at a 29.18% CAGR, Net Income at a 20.64% CAGR, and FCF at a 20.11% CAGR. These growth rates have not been reflected in the stock’s price action. META 0.00%↑ has grown their sales from $40.6 Billion in 2017 to $117.9 Billion in 2021 while still maintaining gross margins > 80%. There are signs business is slowing down a bit, but it is not drying up. 2022 to early 2023 might be a tough year to beat comps from their record year in 2021 but that does not mean their business is going anywhere anytime soon. Their products are sticky, and addicting and, people cannot tear themselves away from their phone screens during the day. This year is a hiccup and to me looks like Apple in 2016 when buffet started buying. Theoretically, META 0.00%↑ has the ability to repurchase roughly 8% of their outstanding shares just with cash on hand.

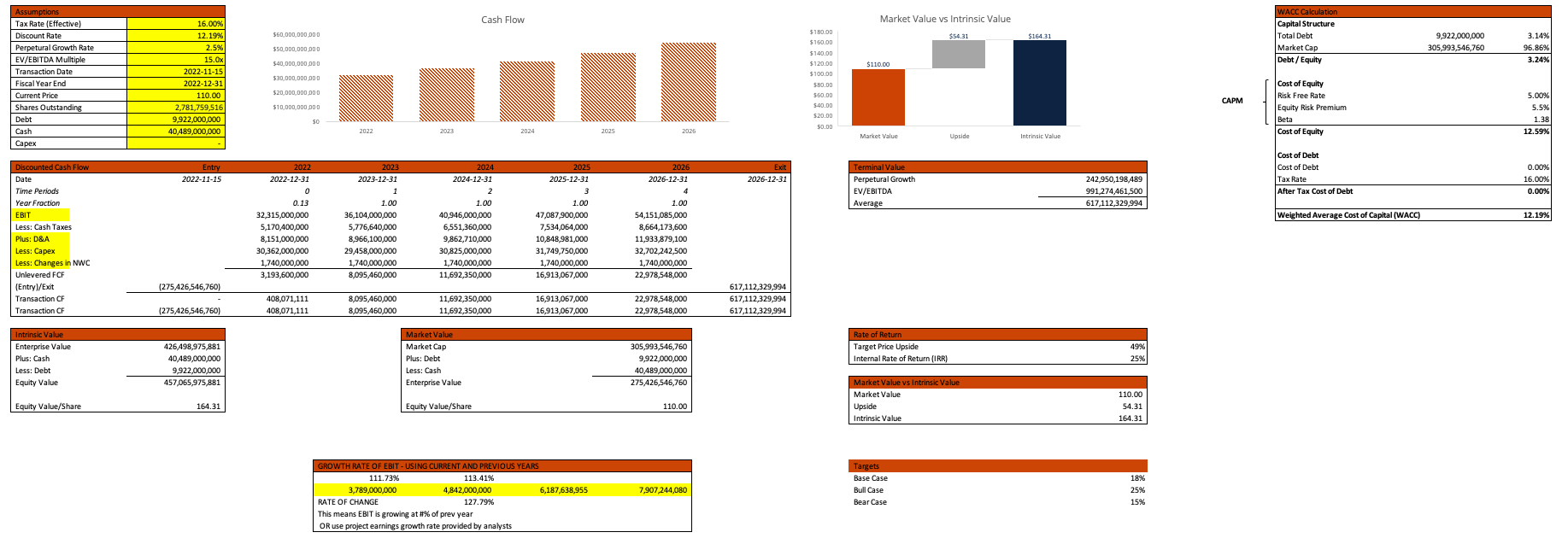

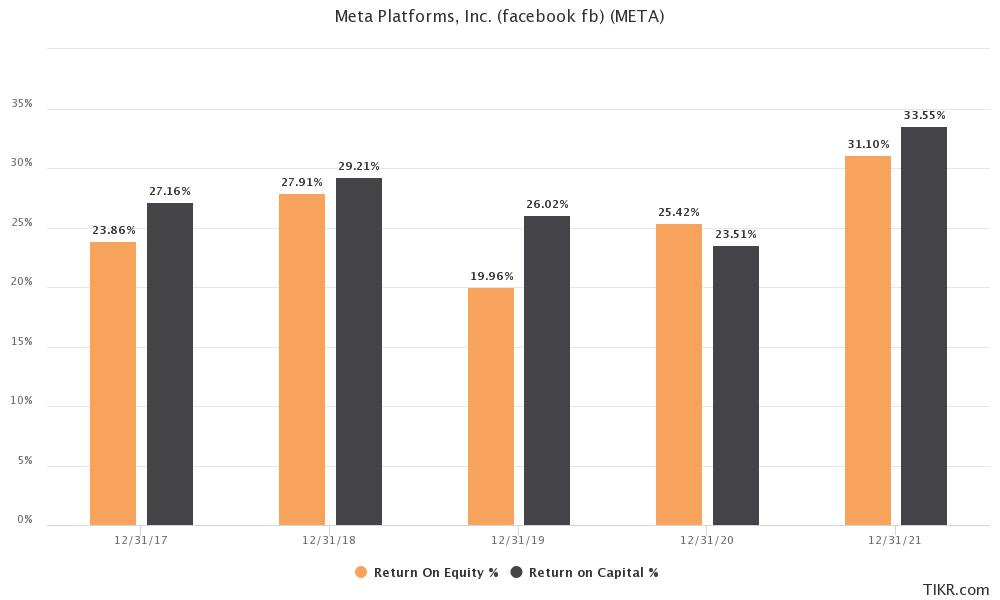

The recent drop in META 0.00%↑’s net income in their ER has made their P/E spike but I first started tweeting about the company when we were trading at a NTM P/E of 13x-14x. At that valuation, it was hard to stop me from constantly buying more. META 0.00%↑’s Historical P/E sits around ~ 23x so for the last 2 months META 0.00%↑ has been trading at a substantial discount. Moreover, their EV/EBITDA has historically been ~ 13x on average compared to 8.8x currently. I have a feeling META 0.00%↑ will be the large cap steal of the year. No other large-cap tech company trades at such a depressed valuation. Relative to other social media/advertising companies META 0.00%↑ has a much higher FCF yield. Being an established company, we can use metrics like ROIC to see how much shareholder wealth they have been able to create over the years. In this category, they are extremely strong and match up to other mega-cap stocks such as GOOG 0.00%↑ and AMZN 0.00%↑. Using my own DCF model with an exit multiple of 15x which I believe is fair for a growing tech company with high margins and relatively low compared to peers, I get a fair value for META 0.00%↑ around $164 which shows upside potential of about 49% from current levels of $110.

Brief Technical Analysis:

To give a technical picture, META 0.00%↑ has recently broken out of the descending wedge. META 0.00%↑’s trend throughout 2022 has been bearish with a lot of selling, but recent weeks show that the trend could be looking to flip bullish. However, we must break through a few resistance levels first before anything can be confirmed. There is a huge gap between 230-300 that could be rapidly filled. The stock seems to have found a floor around $155-$160 which gives me the confidence to say there is more upside than downside from these levels.

Conclusion:

The risks that come with investing in META 0.00%↑ are well understood, there has been a significant level of pessimism which is most likely reflected in the stock price. They still have plenty of time to grow reels and narrow the gap with TikTok. META 0.00%↑ is one of the worst-performing stocks in the S&P 500 in 2022 and its share price seems to be looking for a bottom. The company has faced issues in the short term which will likely continue for the rest of the year. While META 0.00%↑ is not immune to the slowing economy I am confident they will be able to work past Apple’s privacy changes. $40 Billion in cash gives the company the option to buy back shares at discount levels or reinvest it back into the business. The future is bright for META 0.00%↑ with opportunities in Reality Labs and growing monetization in Reels and WhatsApp. My final thought is that if you can ignore the flood of negative headlines about the company and realize the incredible value that META 0.00%↑’s stock is offering you will do very well. Be sure to do your own due diligence. If you enjoyed the read and are interested in more company research like this, please be sure to subscribe to this Substack and share this post with other investors.